For commercial payers, health system pharmacy directors, and market access teams, managing formulary spend requires a dual understanding of a manufacturer’s portfolio. On one side stands the innovative brand portfolio, where upcoming losses of exclusivity (LOE) represent opportunities for significant therapeutic savings. On the other side stands the mature sterile injectables and generic portfolio, where manufacturing bottlenecks, regulatory recalls, and persistent shortages represent severe operational and financial risk.

Few pharmaceutical companies embody this dual-risk profile more clearly than Pfizer Inc. Through its core innovative medicines division and its sterile injectables arm (primarily the Hospira division, acquired in 2015), Pfizer represents both a massive near-term patent cliff target and the single largest supply chain bottleneck in the U.S. hospital market.

This portfolio dossier provides a data-driven regulatory and supply-chain analysis of Pfizer's drug portfolio. Grounded in systematic queries of the FDA Orange Book, FDA Purple Book, FDA Drug Shortages database, FDA Enforcement Reports (recalls), and ClinicalTrials.gov registry, this dossier maps out the upcoming patent cliffs, details the structural shortages of the Hospira division, breaks down Pfizer's historical recall patterns, and provides access teams with concrete risk mitigation frameworks.

Executive Summary & Scenario Analysis

To align on the clinical and economic implications of Pfizer's portfolio transitions, we must address the primary questions facing clinical pharmacy directors, health system purchasing teams, and benefit designers.

Scenario Question

What does public regulatory and supply-chain data reveal about Pfizer's innovative and sterile injectable portfolio, and how should access teams mitigate upcoming patent expirations and shortages?

Direct Answer

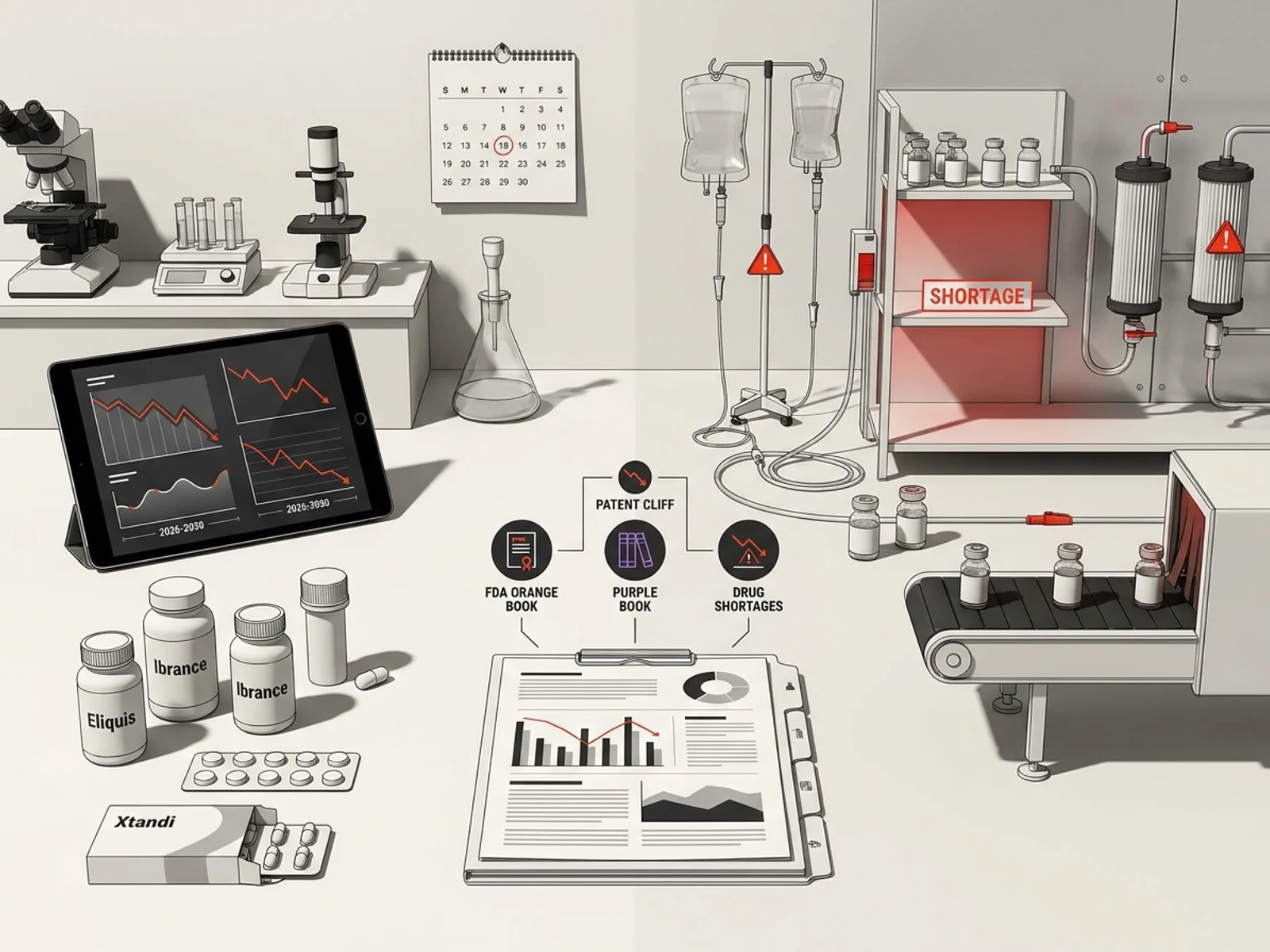

Public regulatory datasets reveal that Pfizer faces a massive innovative patent cliff between 2026 and 2030, with key blockbusters Eliquis (apixaban), Ibrance (palbociclib), Xtandi (enzalutamide), and Xeljanz (tofacitinib) representing over $20B in combined annual revenue facing generic entry. Meanwhile, its sterile injectable division (Hospira) continues to represent the largest supply chain bottleneck in the U.S. hospital market, accounting for 206 shortage listings (165 active as of June 2026) and 165 recalls in the FDA Enforcement database. Access teams must implement therapeutic alternatives for impending LOE products, structure multi-source contracts for sterile injectables, and establish continuous supply monitoring workflows to mitigate facility-driven disruptions.

The Core Product Landscape: Orange Book Insights

Under the Hatch-Waxman Act, the FDA Orange Book (Approved Drug Products with Therapeutic Equivalence Evaluations) serves as the definitive registry for approved small-molecule drug products, their active patents, and regulatory exclusivity periods.

An analysis of the June 10, 2026 FDA Orange Book database snapshot indicates that Pfizer, Hospira, and Pharmacia (a Pfizer subsidiary) collectively hold 1,420 product rows, representing 805 unique approved applications.

This approved application portfolio is split into:

- 341 New Drug Applications (NDAs): Representing Pfizer's history of innovative drug development and brand-name licensing.

- 464 Abbreviated New Drug Applications (ANDAs): Representing the mature sterile injectables, generic small molecules, and institutional hospital products primarily managed under the Hospira division.

This high ratio of ANDAs (57.6% of total approved applications) highlights that while Pfizer is commercially viewed as a branded pharmaceutical innovator, its operational footprint is dominated by generic and mature multi-source products. This structural division splits Pfizer's risk profile: access teams must manage classic brand LOE cliffs for small molecules and vaccines, while simultaneously managing acute supply-chain shortages and quality recalls on the sterile injectables side.

Mapping the 2026-2030 Pfizer Patent Cliff

Between 2026 and 2030, Pfizer faces a highly concentrated patent cliff. Four core blockbusters—representing the pillars of Pfizer's cardiovascular, oncology, and immunology franchises—are scheduled to lose exclusivity or have already entered multi-source generic competition.

For market access teams, tracking these timelines is critical to planning therapeutic transitions, negotiating formulary placement, and project-managing the substitution of high-cost brands. For the wider industry backdrop of how Pfizer's LOE schedule fits into the broader industry schedule, see our analysis of the 2026-2032 patent cliff by the numbers.

1. Eliquis (apixaban)

- Indication: Prevention of stroke in non-valvular atrial fibrillation; treatment and prevention of deep vein thrombosis (DVT) and pulmonary embolism (PE).

- Commercial Partner: Co-developed and co-marketed with Bristol Myers Squibb (BMS).

- Clinical Foundation (The ARISTOTLE Trial): Pfizer and BMS established the clinical profile of apixaban through the landmark ARISTOTLE trial (NCT00412984). This randomized, double-blind, active-controlled Phase III trial evaluated 18,201 patients with non-valvular atrial fibrillation and at least one additional risk factor for stroke. Patients were randomized to receive apixaban (5 mg twice daily) or warfarin (target INR 2.0-3.0). The trial demonstrated that apixaban was statistically superior to warfarin in the primary endpoint of preventing stroke or systemic embolism:

- Stroke/Systemic Embolism: Apixaban achieved a 21% reduction in risk compared to warfarin (HR: 0.79; 95% CI: 0.66–0.95; $p = 0.01$).

- Major Bleeding: Apixaban demonstrated a 31% reduction in major bleeding events (HR: 0.69; 95% CI: 0.60–0.80; $p < 0.001$).

- All-Cause Mortality: Apixaban achieved an 11% reduction in the risk of death from any cause (HR: 0.89; 95% CI: 0.80–0.99; $p = 0.047$).

- Patent Expiration & Exclusivity Status: The core composition-of-matter patent (US Patent No. 6,967,208) expires on November 21, 2026, extended to May 21, 2027 by pediatric exclusivity. A secondary formulation patent (US Patent No. 9,326,945, with its own pediatric exclusivity) runs to August 24, 2031 and was the basis for blocking earlier generic entry. Under patent litigation settlement agreements with generic developers, generic apixaban is permitted to enter the U.S. market on April 1, 2028, bypassing the final years of the formulation patent. The FDA Orange Book lists multiple approved ANDAs (held by MSN, Torrent, Dr. Reddy's, and others) that convert to final approvals on the settlement date.

- Access Implication: Payer formulary exclusion is deferred in the U.S. until 2028. However, international markets (including Europe and Canada) are already experiencing generic apixaban price erosion. Payer teams must maintain current anticoagulation preferences while preparing for rapid conversion in 2028. For details on apixaban's generic delay mechanics, refer to our analysis of the apixaban generic U.S. entry delay.

2. Ibrance (palbociclib)

- Indication: Treatment of HR-positive, HER2-negative advanced or metastatic breast cancer in combination with an aromatase inhibitor or fulvestrant.

- Clinical Foundation (The PALOMA-2 Trial): The therapeutic approval of palbociclib (the first CDK4/6 inhibitor) in the first-line setting was supported by the PALOMA-2 trial (NCT01740427). This randomized, double-blind, placebo-controlled Phase III trial evaluated 666 postmenopausal women with ER-positive, HER2-negative metastatic breast cancer who had not received prior systemic therapy. Patients were randomized to receive palbociclib (125 mg daily on a 3-weeks-on, 1-week-off schedule) plus letrozole (2.5 mg daily) or placebo plus letrozole. Key findings included:

- Progression-Free Survival (PFS): Palbociclib plus letrozole achieved a median PFS of 24.8 months compared to 14.5 months in the placebo-letrozole arm (HR: 0.58; 95% CI: 0.46–0.72; $p < 0.001$), representing a 10.3-month clinical extension in disease control.

- Objective Response Rate (ORR): The palbociclib combination demonstrated an ORR of 55.3% in patients with measurable disease compared to 44.4% in the control group.

- Patent Expiration & Exclusivity Status: The compound patent (US Patent No. 6,936,612) and its associated pediatric exclusivity are set to expire in the United States in January 2027. While Pfizer has secured formulation and method-of-use patents extending into the 2030s (including US Patent No. 10,723,730 covering specific tablet formulations), generic challenges are active. Payers should anticipate the earliest generic palbociclib market entry between 2027 and 2028, depending on the resolution of outstanding Paragraph IV litigation.

- Access Implication: Palbociclib is currently billed under the specialty pharmacy benefit. Payer teams should expect generic entry to trigger rapid prior authorization shifts. Because generic palbociclib will launch into a competitive therapeutic class (alongside Novartis's Kisqali and Eli Lilly's Verzenio), the generic launch will exert downward price pressure on the entire CDK4/6 inhibitor class.

3. Xtandi (enzalutamide)

- Indication: Treatment of castration-resistant prostate cancer (CRPC) and metastatic castration-sensitive prostate cancer (mCSPC).

- Commercial Partner: Co-developed and co-marketed with Astellas Pharma.

- Clinical Foundation (The PREVAIL Trial): Enzalutamide's expansion into chemo-naive metastatic prostate cancer was driven by the landmark PREVAIL trial (NCT01212991). This randomized, double-blind, placebo-controlled Phase III trial evaluated 1,717 patients with asymptomatic or mildly symptomatic metastatic CRPC. Patients received enzalutamide (160 mg daily) or placebo. Key outcomes included:

- Radiographic Progression-Free Survival (rPFS): Enzalutamide demonstrated an 81% reduction in the risk of radiographic progression or death (HR: 0.19; 95% CI: 0.15–0.23; $p < 0.0001$).

- Overall Survival (OS): Enzalutamide achieved a statistically significant 29% reduction in the risk of death (HR: 0.71; 95% CI: 0.60–0.84; $p < 0.0001$).

- Time to Chemotherapy Initiation: Enzalutamide delayed the median time to the initiation of cytotoxic chemotherapy to 28.0 months compared to 10.8 months in the placebo arm.

- Patent Expiration & Exclusivity Status: The core formulation and method-of-use patents (including US Patent No. 7,709,517) are scheduled to expire in the United States in 2027. The FDA has already granted tentative approvals to several generic enzalutamide ANDAs (including applications from Apotex, Watson, and Sandoz). Actual generic launch is expected in mid-to-late 2027.

- Access Implication: Xtandi represents a multi-billion-dollar driver of oncology pharmacy spend. Payers must monitor the enzalutamide generic runway, as the transition to generic alternatives will yield immediate savings of 80% to 90% within the first 180 days of multi-source entry.

4. Xeljanz / Xeljanz XR (tofacitinib)

Indication: Treatment of rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, and ulcerative colitis.

Clinical Foundation (ORAL Solo and ORAL Scan): Tofacitinib (the first approved JAK inhibitor for rheumatoid arthritis) was evaluated in several pivotal trials:

- ORAL Solo (NCT00814307): This randomized, double-blind, placebo-controlled Phase III trial evaluated 611 patients with active rheumatoid arthritis who had an inadequate response to at least one disease-modifying antirheumatic drug (DMARD). Patients received tofacitinib monotherapy (5 mg or 10 mg twice daily) or placebo. Tofacitinib achieved statistically superior ACR20 response rates at Month 3, reaching 59.8% in the 5 mg arm and 65.7% in the 10 mg arm, compared to just 26.7% in the placebo group (p < 0.0001).

- ORAL Scan (NCT00847613): This Phase III trial evaluated 799 patients with active rheumatoid arthritis receiving a stable background dose of methotrexate. Tofacitinib (5 mg or 10 mg twice daily) plus methotrexate demonstrated significant improvements in physical function and statistically significant reductions in the progression of structural joint damage (as measured by the modified Total Sharp Score) compared to placebo plus methotrexate at Month 6.

The Safety Gate (The ORAL Surveillance Trial): Due to concerns regarding lipid elevations and potential malignancy signals during development, the FDA mandated a large-scale post-marketing safety study. The ORAL Surveillance trial (NCT02092463) was a randomized, active-controlled, open-label trial that evaluated 4,362 patients aged 50 years and older with active rheumatoid arthritis and at least one additional cardiovascular risk factor. Patients received tofacitinib (5 mg or 10 mg twice daily) or a TNF inhibitor (adalimumab or etanercept). Key safety findings included:

- Major Adverse Cardiovascular Events (MACE): Tofacitinib failed to meet non-inferiority criteria compared to TNF inhibitors. The hazard ratio for tofacitinib (combined doses) vs. TNF inhibitors was 1.33 (95% CI: 0.91–1.94), showing a higher incidence of myocardial infarction and stroke.

- Malignancies: Tofacitinib demonstrated a higher incidence of cancers (excluding non-melanoma skin cancer), with a hazard ratio of 1.48 (95% CI: 1.04–2.09), showing increased rates of lung cancer and lymphoma.

- Thromboembolic Events: A higher rate of pulmonary embolism and deep vein thrombosis was observed in the tofacitinib arms, particularly in patients receiving the 10 mg twice daily dose, which led the FDA to restrict the 10 mg strength to ulcerative colitis indications only.

These findings resulted in the FDA adding a class-wide boxed warning to all JAK inhibitors regarding the risks of serious heart-related events, cancer, blood clots, and death.

Patent Expiration & Exclusivity Status: The basic active ingredient patent for tofacitinib (US Patent No. 7,301,023) expired in December 2025. While Pfizer continues to defend secondary patents covering the extended-release formulation (Xeljanz XR, covered by patents extending to 2034), generic versions of the immediate-release tablet (5 mg and 10 mg) have entered the U.S. market as of late 2025 and early 2026.

Access Implication: Xeljanz has experienced steady commercial decline due to class-wide FDA boxed warnings regarding JAK inhibitor safety (including thromboembolic events and malignancy risks). Payers should leverage generic immediate-release tofacitinib to implement step-therapy requirements, mandating generic tofacitinib before allowing brand-name JAK inhibitors (such as AbbVie's Rinvoq or Pfizer's Cibinqo) for rheumatoid arthritis and ulcerative colitis.

The table below summarizes the commercial and regulatory status of Pfizer's primary LOE cliff products:

| Brand Name | Active Ingredient | Primary Therapeutic Area | Key U.S. Patent Expiration | Expected Generic Entry Date | FDA Orange Book Patent Count |

|---|---|---|---|---|---|

| Xeljanz | Tofacitinib Citrate | Immunology / Rheumatology | Dec 2025 (Expired) | Active (Early 2026) | 3 (Secondary patents remaining) |

| Ibrance | Palbociclib | Oncology (CDK4/6) | Jan 2027 | 2027–2028 (P-IV pending) | 8 (Formulation & dosing) |

| Xtandi | Enzalutamide | Oncology (Prostate) | May 2027 | Mid-2027 | 6 (Formulation & use) |

| Eliquis | Apixaban | Cardiovascular (Anticoagulant) | Nov 2026 (Core) | April 1, 2028 (Settlement) | 12 (Formulation, use & salt) |

Supply Chain Risks: The Hospira Sterile Injectables Shortage Profile

While innovative drug patents represent a commercial planning challenge, Pfizer's generic sterile injectable portfolio represents an active operational risk. Pfizer’s sterile injectable division, operating under the Hospira label, is the largest supplier of generic injectable medications to U.S. hospitals.

Sterile injectables (including emergency anesthetics, neuromuscular blockers, electrolytes, and anti-infectives) are highly sensitive to manufacturing disruptions. Because they are administered intravenously or intramuscularly, they must be manufactured in highly sterile environments under strict Current Good Manufacturing Practice (cGMP) regulations.

Quantifying the Shortage Footprint

An analysis of the June 10, 2026 FDA Drug Shortages database snapshot reveals that Hospira, Inc. (a Pfizer Company) accounts for 206 shortage records.

This shortage profile is categorized as follows:

- 165 Current Active Shortages: Injectable formulations currently unavailable or in severely restricted distribution from Hospira facilities.

- 7 Resolved Shortages: Products where normal supply lines were restored in the current quarter.

- 34 To Be Discontinued: Mature sterile injectable lines that Pfizer has flagged for retirement, typically due to low margins, active ingredient unavailability, or the need to reallocate sterile manufacturing capacity to higher-priority lines.

In comparison, Pfizer's core brand division accounts for 91 shortage records (43 current active shortages and 48 flagged as to be discontinued). This indicates that the vast majority of Pfizer's supply-chain vulnerability is concentrated in the Hospira division, specifically within generic sterile injectables.

For health system pharmacy operations, these numbers are not abstract metrics. They represent clinical bottlenecks where pharmacy staff must compound alternatives, purchase higher-cost brand equivalents, or implement therapeutic substitution protocols. To understand the wider system-level impact of these events, refer to the FDA drug shortage list and reading workflows.

The Rocky Mount Bottleneck: A Single Point of Failure

The core of Hospira's sterile injectable manufacturing footprint is located in Rocky Mount, North Carolina. This facility is one of the largest sterile injectable plants in the world, historically responsible for manufacturing nearly 25% of all sterile injectables used in U.S. hospitals.

The Rocky Mount site has a history of regulatory and environmental challenges:

- FDA Warning Letters: Under Hospira's original management, the Rocky Mount facility received multiple FDA warning letters (including a comprehensive warning letter in 2010) citing critical cGMP failures. These included inadequate sterility assurance, particulate contamination (such as metal and glass fragments in vials), and poor investigation of product complaints. Pfizer invested heavily in remediation following its 2015 acquisition, resulting in the FDA lifting the warning letter status.

- Product Recalls: Despite remediation, the facility’s scale and age have resulted in recurring voluntary recalls. These are typically driven by particulate matter found in single-dose vials or issues with container closure integrity.

- The July 2023 Tornado: The facility's supply-chain vulnerability was highlighted on July 19, 2023, when an EF-3 tornado directly struck the Rocky Mount site. The tornado caused severe damage to the facility's warehouse, which stored thousands of pallets of finished pharmaceuticals awaiting distribution. While the sterile production lines themselves escaped structural destruction, the loss of warehouse inventory triggered immediate, acute shortages of critical injectables across the United States, including bupivacaine, lidocaine, fentanyl, potassium chloride, and sodium chloride infusions.

The table below outlines the recovery timeline and regulatory steps following the 2023 tornado event:

| Milestone / Phase | Operational Date | Description of Sourcing Actions & Facility Status | Key Shortage Consequences |

|---|---|---|---|

| Tornado Strike | July 19, 2023 | EF-3 tornado heavily damages the Rocky Mount warehouse. Production is immediately halted. | Immediate supply constraints on bupivacaine, lidocaine, and saline. |

| Phased Restart | Q4 2023 | Pfizer begins limited restart of manufacturing lines under FDA observation. | Group purchasing organizations (GPOs) institute allocation controls. |

| Warehouse Restore | Early 2024 | Replacement warehouse facilities become operational; production lines reach 80% capacity. | Emergency ordering processes modified; partial resolution of anesthesia shortages. |

| Full Capacity | Late 2024 | Rocky Mount returns to normal operational capacity with updated warehouse security and quality monitoring. | Stabilized national supply lines for core sterile electrolytes and anesthetics. |

Sourcing Decision Rule for Health System Buyers

To mitigate the operational risk of Hospira-centered sterile injectable shortages, hospital purchasing coalitions and group purchasing organizations (GPOs) must implement the following Sourcing Decision Matrix:

[Is the Injectable Molecule Monosourced to Hospira?]

|

+---> YES: Establish 3-Month Safety Stock + Contract with 503B Outsourcing Facility

|

+---> NO: Implement Dual-Sourcing Contract (e.g., 60% Hospira / 40% Fresenius Kabi or Hikma)

- Dual-Sourcing Mandates: GPOs should avoid signing 100% sole-source contracts with Hospira for critical institutional molecules. Contracts should be structured as dual-source (e.g., a 60/40 volume split between Hospira and competitors like Fresenius Kabi, Hikma, or Baxter) to ensure secondary supply lines remain active.

- 503B Compounding Partnerships: For molecules where Hospira holds a dominant market share (such as specific packaging formats of emergency anesthetics), hospitals should establish active accounts with registered 503B outsourcing facilities to secure compounded sterile preparations during acute manufacturer shortages.

Pfizer's FDA Recall History: Operational Quality Analysis

A manufacturer's recall history is a leading indicator of manufacturing quality and supply-chain resilience. In biopharma, product recalls are classified by the FDA based on the severity of the hazard:

- Class I Recalls: Dangerous or defective products that predictably cause serious health problems or death.

- Class II Recalls: Products that might cause a temporary health problem or pose a slight risk of a serious nature.

- Class III Recalls: Products unlikely to cause any adverse health reaction but violate FDA labeling or manufacturing laws.

An analysis of the June 10, 2026 FDA Enforcement database snapshot reveals 309 mutually-exclusive recall records naming a Pfizer-associated entity:

- Hospira, Inc. Recalls: 165 records (12 of which are filed under the combined "Hospira, Inc., a Pfizer Company" label)

- Pfizer Core Recalls (brand division, excluding Hospira): 143 records

- Pharmacia & Upjohn / Parke-Davis (legacy subsidiaries): 1 record

This breakdown shows that Hospira represents a disproportionate share of Pfizer's regulatory quality events. While Hospira and Pfizer core have comparable total recall counts (165 vs 143), Hospira's recalls are almost entirely concentrated in sterile injectable products, where the clinical risk of particulate contamination or sterility failure is significantly higher than for oral solids.

Key Quality Failure Categories in Hospira Injectables

A review of the narrative descriptions in the FDA Enforcement database identifies three recurring root causes for Hospira's sterile recalls:

- Particulate Contamination: The presence of foreign matter—such as glass particles, stainless steel fragments, or silicone fibers—inside sealed glass vials or syringes. Injecting particulate matter can cause local vascular irritation, pulmonary emboli, or systemic inflammatory responses.

- Sterility Assurance Failures: Observations of sub-sterile conditions in the manufacturing line, such as environmental monitoring deviations or failures in media fills. These recalls are typically voluntary, precautionary measures taken before actual contamination is reported.

- Container Closure Integrity Issues: Cracks in glass vials, leaking syringe plungers, or incomplete crimping of aluminum caps. Any compromise in the container closure barrier allows microbial ingress, rendering the sterile injectable unsafe for clinical use.

The table below catalogs specific historical recall cases for Pfizer and Hospira to demonstrate typical root-cause findings:

| Recalling Firm | Product / Active Ingredient | BLA/NDA/ANDA Number | Recall Class | Core Root-Cause Finding |

|---|---|---|---|---|

| Hospira Inc. | Sodium Bicarbonate Injection | ANDA 077394 | Class II | Presence of glass particulate matter inside the vial. |

| Hospira Inc. | Heparin Sodium Injection | ANDA 040095 | Class II | Sterility assurance failure due to mold detected in the cleanroom environment. |

| Pfizer Inc. | Bicillin L-A (Penicillin G Benzathine) | NDA 050141 | Class II | Presence of visible crystalline particulate matter in the suspension syringes. |

| Hospira Inc. | Carboplatin Injection | ANDA 076473 | Class II | Visible particulate matter identified during stability testing. |

| Hospira Inc. | Lidocaine HCl Injection | ANDA 040013 | Class II | Container closure integrity compromise due to defective rubber stoppers. |

Purple Book Biologics: Biosimilars and Reference Portfolio

As the biopharmaceutical market shifts from small-molecule generics to large-molecule biologics, the FDA Purple Book (Database of Licensed Biological Products) has become central to market access planning. Biologics are approved under two pathways:

- 351(a) BLA Pathway: The standard pathway for original, reference biological products.

- 351(k) BLA Pathway: The pathway for biosimilar and interchangeable biological products.

An analysis of the June 10, 2026 FDA Purple Book database snapshot indicates that Pfizer-associated entities (including Pfizer Inc., Pfizer Ireland Pharmaceuticals, and Hospira Inc.) hold 20 unique Biological License Applications (BLAs).

This biological portfolio is split into:

- 12 Reference Biologics (351(a)): Original innovative biologics, including Abrysvo (respiratory syncytial virus vaccine, BLA 125769), Elrexfio (elranatamab-bcmm, BLA 761345), BEQVEZ (fidanacogene elaparvovec-dzkt, BLA 125786), Ngenla (somatrogon-ghla, BLA 761184), Hympavzi (marstacimab-hncq, BLA 761369), and PENBRAYA (meningococcal groups A/B/C/W/Y vaccine, BLA 125770), alongside legacy Pharmacia & Upjohn reference products such as Genotropin (somatropin, BLA 20280), Somavert (pegvisomant, BLA 21106), Atgam (lymphocyte immune globulin, BLA 103676), Elelyso (taliglucerase alfa, BLA 22458), and Ticovac (tick-borne encephalitis vaccine, BLA 125740).

- 8 Biosimilars (351(k)): Replicas of blockbuster reference biologics, including Retacrit (epoetin alfa-epbx, BLA 125545), Ruxience (rituximab-pvvr, BLA 761103), Zirabev (bevacizumab-bvzr, BLA 761099), Trazimera (trastuzumab-qyyp, BLA 761081), and Abrilada (adalimumab-afzb, BLA 761118).

Note on corporate taxonomy: If the analysis is expanded to include all historic Pfizer acquisitions and legacy entities (such as Wyeth Pharmaceuticals and Pharmacia & Upjohn), the BLA count rises to 32 unique licenses (24 reference biologics and 8 biosimilars). This reflects Pfizer's acquisition-driven expansion, which brought blockbusters like Benefix (coagulation factor IX, BLA 103677) and the Prevnar pneumococcal vaccine franchise under Pfizer's regulatory umbrella.

Pfizer's Biosimilar Footprint

Pfizer's biosimilar division represents a successful execution of the 351(k) pathway. By launching biosimilars for key oncology and immunology reference biologics, Pfizer has established a strong presence in the specialty pharmacy space.

The table below maps Pfizer's 8 approved biosimilars, their reference products, and their regulatory status:

| Biosimilar Brand | Active Ingredient | Reference Biologic | Target Indication | BLA Number | Pathway / Exclusivity Status |

|---|---|---|---|---|---|

| Retacrit | Epoetin alfa-epbx | Epogen / Procrit | Anemia (chronic kidney disease/oncology) | BLA 125545 | 351(k) Biosimilar |

| Nivestym | Filgrastim-aafi | Neupogen | Neutropenia prevention | BLA 761080 | 351(k) Biosimilar |

| Nyvepria | Pegfilgrastim-apgf | Neulasta | Neutropenia prevention | BLA 761111 | 351(k) Biosimilar |

| Trazimera | Trastuzumab-qyyp | Herceptin | HER2+ Breast/Gastric Cancer | BLA 761081 | 351(k) Biosimilar |

| Zirabev | Bevacizumab-bvzr | Avastin | Colorectal/Lung/Glioblastoma Cancer | BLA 761099 | 351(k) Biosimilar |

| Ruxience | Rituximab-pvvr | Rituxan | Non-Hodgkin Lymphoma, CLL, RA | BLA 761103 | 351(k) Biosimilar |

| Ixifi | Infliximab-qbtx | Remicade | Rheumatoid Arthritis, Crohn's, UC | BLA 761072 | 351(k) Biosimilar |

| Abrilada | Adalimumab-afzb | Humira | Rheumatoid Arthritis, Plaque Psoriasis, Crohn's | BLA 761118 | 351(k) Interchangeable |

The Case of Abrilada: Interchangeability in Action

Abrilada (adalimumab-afzb) is a key case study in biologic market access. While originally approved in 2019, it was subsequently granted the interchangeable designation by the FDA, making it one of the early interchangeable Humira biosimilars (after Boehringer Ingelheim's Cyltezo). Interchangeability allows pharmacists to substitute Abrilada for the reference product, Humira, without the intervention of the prescribing healthcare provider, subject to state pharmacy laws.

To secure market share, Pfizer positioned Abrilada with a dual-pricing strategy:

- High-List/High-Rebate Option: Matching Humira's Wholesale Acquisition Cost (WAC) to appeal to PBMs that prefer high-rebate structures to pad their administrative fees.

- Low-List/No-Rebate Option: Offered at a discount of over 80% to Humira's WAC, targeting health systems, independent plans, and cash-pay models that prioritize direct, transparent savings.

Payer formulary directors must leverage these dual-pricing options to evaluate their total net cost. If a plan is highly rebate-dependent, the high-list version may yield higher cosmetic savings. If a plan is self-funded or structured as a pass-through entity, the low-list option provides immediate, clean savings at the point of sale.

Clinical Development Intensity and R&D Focus

To replace the revenue lost during the 2026-2030 patent cliff, Pfizer is maintaining an active clinical pipeline. An analysis of the ClinicalTrials.gov registry snapshot from June 10, 2026 indicates that Pfizer sponsored:

- 111 Clinical Trials starting in 2024

- 111 Clinical Trials starting in 2025

- 53 Clinical Trials starting in the first half of 2026

This consistent trial volume (averaging 111 new trials annually for the past two years) indicates that Pfizer is actively feeding its pipeline to offset LOE erosion.

Core R&D Segments

Pfizer's active trials are concentrated in three primary therapeutic areas:

Oncology: Following its $43 billion acquisition of Seagen in late 2023, Pfizer has redirected its clinical focus toward Antibody-Drug Conjugates (ADCs). The pipeline contains multiple Phase II and Phase III trials evaluating next-generation ADCs targeting solid tumors, including breast, lung, and urothelial cancers.

A primary clinical asset in this category is Padcev (enfortumab vedotin-ejfv), an ADC targeting Nectin-4 which is co-developed with Astellas. The therapeutic expansion of Padcev into first-line advanced urothelial cancer was supported by the landmark EV-302 Phase III trial (NCT04723745). This randomized, open-label trial evaluated 886 patients with previously untreated locally advanced or metastatic urothelial cancer. Patients were randomized to receive enfortumab vedotin in combination with pembrolizumab (Keytruda) or standard platinum-based chemotherapy (gemcitabine plus cisplatin or carboplatin). Key findings included:

- Progression-Free Survival: The Padcev combination achieved a median PFS of 12.5 months compared to 6.3 months in the chemotherapy control arm, representing a 53% reduction in the risk of disease progression or death (HR: 0.45; 95% CI: 0.38–0.54; $p < 0.0001$).

- Overall Survival: The combination demonstrated a statistically significant survival benefit, reaching a median OS of 31.5 months vs. 16.1 months in the control group (HR: 0.47; 95% CI: 0.38–0.58; $p < 0.0001$), effectively doubling median overall survival for this patient population.

Vaccines: Capitalizing on its mRNA infrastructure, Pfizer has active trials for combination respiratory vaccines (e.g., combination Covid-19/influenza vaccine lines) and next-generation pneumococcal conjugate vaccines.

Immunology & Inflammation: Focusing on oral small molecules (such as JAK inhibitors and TYK2 inhibitors) and bispecific antibodies to secure long-term immunology revenue.

Market access teams should monitor Pfizer’s Phase III trials, particularly in oncology and immunology, as successful readouts will lead to new, high-cost specialty drug approvals. Payer teams must begin planning utilization management criteria (prior authorization and biomarker requirements) 12 to 18 months before expected FDA approval.

FAQ Section

When are generic versions of Eliquis, Ibrance, and Xeljanz expected to launch?

- Xeljanz (tofacitinib): Generic versions of the immediate-release tablet (5 mg and 10 mg) entered the U.S. market in late 2025 and early 2026. Extended-release (Xeljanz XR) generics remain delayed due to outstanding patent protections.

- Ibrance (palbociclib): The earliest generic market entry is expected in January 2027 upon the expiration of the core compound patent and pediatric exclusivity, subject to the resolution of pending Paragraph IV litigation.

- Eliquis (apixaban): Following patent litigation settlements, generic apixaban is scheduled to enter the U.S. market on April 1, 2028.

Why are so many Pfizer shortages concentrated in the Hospira division?

The Hospira division manufactures sterile injectables (such as anesthetics, electrolytes, and anti-infectives). These formulations require highly sterile, complex production environments that are vulnerable to contamination, sterility assurance failures, and strict cGMP regulatory actions. Additionally, mature generic injectables carry low profit margins, leading manufacturers to run facilities at capacity with minimal safety stock, exacerbating supply-chain vulnerabilities.

How does Pfizer's sterile injectable recall profile compare to its brand-name innovative drugs?

Hospira accounts for 165 recalls in the FDA Enforcement database, while Pfizer core accounts for 143 recalls. While the total counts are similar, Hospira's recalls are concentrated in injectables and are frequently Class II recalls driven by sterility assurance risks, particulate contamination, and container closure failures. Pfizer core recalls are primarily driven by labeling errors or secondary tablet packaging issues.

What biosimilars does Pfizer market in the United States?

Pfizer markets 8 biosimilars approved under the 351(k) pathway: Retacrit (epoetin alfa-epbx), Nivestym (filgrastim-aafi), Nyvepria (pegfilgrastim-apgf), Trazimera (trastuzumab-qyyp), Zirabev (bevacizumab-bvzr), Ruxience (rituximab-pvvr), Ixifi (infliximab-qbtx), and Abrilada (adalimumab-afzb). Abrilada is approved as an interchangeable biosimilar to Humira.

Sources

- FDA Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. June 10, 2026 snapshot. https://www.accessdata.fda.gov/scripts/cder/ob/index.cfm

- FDA Purple Book: Database of Licensed Biological Products. U.S. Food and Drug Administration. June 10, 2026 snapshot. https://purplebooksearch.fda.gov/

- FDA Drug Shortages Database. U.S. Food and Drug Administration. June 10, 2026 snapshot. https://www.fda.gov/drugs/drug-safety-and-availability/drug-shortages

- FDA Enforcement Reports: Recalls and Market Withdrawals. U.S. Food and Drug Administration. June 10, 2026 snapshot. https://www.fda.gov/safety/recalls-market-withdrawals-safety-alerts

- ClinicalTrials.gov Registry Database. National Institutes of Health / National Library of Medicine. June 10, 2026 snapshot. https://clinicaltrials.gov/

- Pfizer Inc. Form 10-K Annual Report for the fiscal year ended December 31, 2025. Filed with the U.S. Securities and Exchange Commission on February 26, 2026. Intellectual Property and Supply Chain Risk Disclosures. https://www.sec.gov/edgar/searchedgar/companysearch.html

- Centers for Medicare & Medicaid Services (CMS). National Average Drug Acquisition Cost (NADAC) Files, database update dated June 10, 2026. https://www.medicaid.gov/medicaid/prescription-drugs/pharmacy-pricing/index.html